Manufactured Homes Get a 'Game Changing' Boost in Federal Housing Push

Housing—and the urgent need for more of it, at more affordable prices—scored prime real estate in President Biden’s State of the Union address in March, as the president proposed tax credits for first-time home buyers, sellers of starter homes, and affordable housing developers.

But there’s more to the Biden-Harris Administration’s latest housing plan than was mentioned in the president’s speech—including three big actions to bolster manufactured housing, which is already the most abundant source of unsubsidized affordable housing in the United States. Factory-built homes offer a cost-efficient and speedy option to ramp up production of the smaller, entry-level homes America sorely needs to meet its housing demand.

The White House’s positioning of manufactured housing among its solutions to the nation’s affordable housing woes is extraordinary, says Arica Young, associate director of the Innovations in Manufactured Homes (I’m HOME) Network, a group convened by the Lincoln Institute of Land Policy that promotes manufactured housing as a safe and affordable path to homeownership.

The administration’s attention and the new federal moves—which include establishing a grant program for manufactured housing communities, increasing borrowing limits for individuals, and offering a new financing approach for resident cooperatives—could go a long way toward reversing lingering stereotypes and stigma associated with manufactured homes, Young says: “I think it's game changing, to be perfectly honest. It's taking a form of housing that was viewed as a last resort and discussing it as a viable option.”

Grants for Manufactured Housing Communities

The first new initiative will award $225 million in competitive grants to manufactured housing communities (MHCs) to make infrastructure improvements or to repair or replace dilapidated homes. Manufactured housing communities, colloquially known as mobile home parks, generally must fund and maintain their own infrastructure, from roads and sidewalks to water and sewer services. And in many MHCs, these vital systems are long overdue for upgrades.

“It's really expensive, and owners don't always have the incentive or the money to keep up with the infrastructure or repairs,” says Young. “A lot of older facilities are mom-and-pop–owned, and they've been run on shoestring budgets. And in some cases, they've forced in more units than the infrastructure can accommodate.”

Grants awarded through the new Preservation and Reinvestment Initiative for Community Enhancement (PRICE) program can be used to fund the installation or improvement of such critical infrastructure, as well as the repair or replacement of existing manufactured homes, energy efficiency or accessibility updates, resiliency measures, and environmental remediation, among other improvements. Notably, homes manufactured before the Department of Housing and Urban Development (HUD) standardized its building code in 1976 are not eligible for repairs, only replacement.

“PRICE is a completely new program. It's exciting because it’s the first time that this money has been specifically appropriated for infrastructure improvements in manufactured housing communities and the replacement of pre-1976 manufactured homes,” says Maya Hamberg, policy analyst at the Lincoln Institute. Communities can also use the funds to help existing residents acquire the land they’re renting, or to prepare lots for new manufactured housing—running new utility and water lines, for example.

The bulk of the grant money, $200 million, “is for broad use by state and local governments, multi-jurisdictional entities, cooperatives, nonprofits, resident-owned communities, CDFIs [community development financial institutions], and tribal applicants,” Hamberg says. A portion of that funding, $10 million, is designated specifically for applicants from federally recognized tribes, who can also apply for the maximum grant of up to $75 million.

The final $25 million will fund a pilot program that uses manufactured homes as an affordable replacement housing strategy in MHCs, swapping old mobile homes in disrepair with up to four new units. In a state like Arizona, Hamberg says, where nearly a third of manufactured homes predate the mid-1970s standardized HUD code, “a community with a preponderance of these homes could apply for a matching grant through PRICE” to replace deteriorating structures with efficient but affordable new ones.

Raising Awareness, and Loan Limits

Replacing more pre-1976 mobile homes with today’s well-built, energy-efficient models won’t just improve living conditions and resiliency for those homeowners; it could also help change public perception, Young says. “This is not your grandfather's mobile home. They're high-quality homes, and they can be as resilient as site-built houses in disasters, if not more so, depending on what part of the HUD code they meet. But there's still a lot of stigma, and education we need to do to overcome that stigma.”

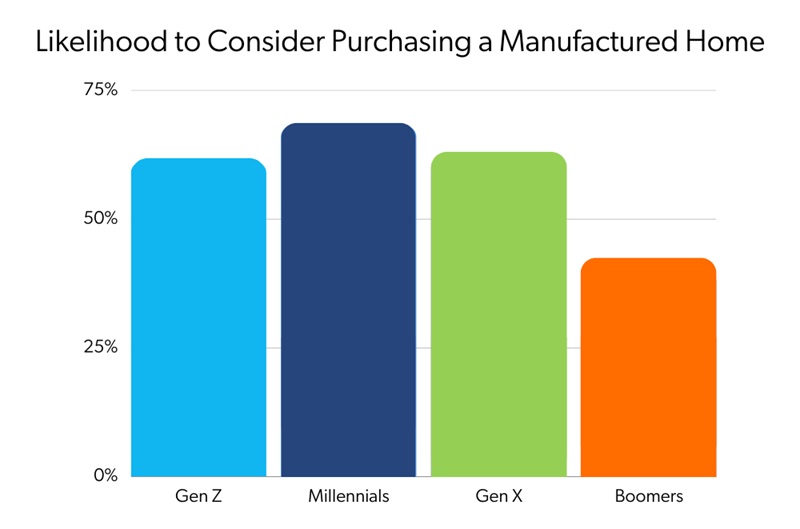

It’s not necessarily homebuyers who hold a negative perception of manufactured homes. A 2022 survey by Freddie Mac found that over 60 percent of respondents across racial and income demographics—and more than two-thirds of millennials—would consider buying a manufactured home.

But lenders, lawmakers, and zoning officials still seem to turn up their noses at manufactured housing, which limits the availability and accessibility of the housing type. As Lincoln Institute President and CEO George W. McCarthy said in his 2022 testimony before a Congressional subcommittee, “Although manufactured homes have reached the same quality as site-built homes, they hold a second-class status in our financial and legal systems.”

More than 40 percent of manufactured homes are not titled as “real property” under state laws, for example, and therefore don’t qualify for a mortgage. That leaves manufactured homebuyers to rely on personal property (or “chattel”) loans with shorter terms and higher interest rates—and nearly two-thirds of those applications are denied, partly due to stricter credit standards and a dearth of participating lenders.

What’s more, until this month, the borrowing limit on the FHA’s personal property loan program, Title I, hadn’t been updated since 2008, rendering the loan program functionally useless. The average price of a new double-section manufactured home was roughly $150,000 in 2023, not including the cost of land or site preparation; the maximum loan the FHA would back was just $69,678.

The administration’s second major action on manufactured housing aims to remedy that. In a new rule change that took effect March 29—one that the I’m HOME Network has long been advocating for—the FHA increased its Title I borrowing limits to 115 percent of the average price of a new manufactured home. That will allow a manufactured home buyer to borrow upwards of $105,000 for a single-section unit, and nearly $200,000 for a double-section home. “In addition to raising the loan limits, the rule also provides for annual indexing, so they don't have to do this again in 10 years when the loan limits are outdated,” Young says.

FHA Financing for Resident Ownership

A third win for manufactured housing in the newly announced plan is a proposed change at the Federal Housing Administration (FHA) that will allow resident cooperatives to use an FHA 223(f) multifamily loan to acquire or refinance their manufactured home community.

Resident ownership is one way for manufactured housing communities to remain affordable—and out of the hands of profit-focused investors, who have been known to scoop up MHCs and abruptly jack up the rents on longtime residents who lease the land beneath their home. However, securing financing for such a purchase can prove difficult for a group of residents.

“There's just a lack of financing available writ large for resident-owned communities, especially government-backed programs that insure lenders against losses on mortgage defaults,” Young says. “So this is another avenue for borrowers to apply for these loans that otherwise wouldn't have been available to them.”

Local Barriers Remain

While the administration’s actions are heartening, there’s still much to do, at both the federal and local levels, before manufactured homes can play a bigger role in easing our housing crisis. Exclusive zoning rules and other land use restrictions remain a major barrier to the greater use of manufactured housing for entry-level homeownership, for example, according to a new report by Harvard’s Joint Center for Housing Studies.

But there are encouraging signs that city officials and zoning boards are starting to come around, too, Young says.

“If you go to planning sessions, city planners are dying to find out about manufactured housing,” she says. “Nobody ever talked about manufactured housing as infill, but they are now. Not a lot of people have talked about manufactured housing as multilevel, but they are now, and they’re discussing the technical feasibility around that.”

In addition to educating the public and policymakers about manufactured housing, members of the I’m HOME Network have met with government officials and other institutions to discuss ways of leveraging the efficiency and affordability of the housing type.

McCarthy’s testimony before the subcommittee and the information he provided was “instrumental in helping them make a supportive decision on how much to allot toward the PRICE Act especially, but also to highlight some of the inherent structural issues with both resident-owned communities and manufactured housing writ large,” Young says.

In February, members of the I’m HOME Network and the Pew Charitable Trusts cohosted a meeting with housing officials in Washington, DC, Hamberg says. “The focus was specifically on Title I, to talk through with HUD officials and other leading experts in the manufactured housing field what is important about these changes—but also what more needs to be done.”

Jon Gorey is a staff writer at the Lincoln Institute of Land Policy.

Lead image: Manufactured housing is gaining attention as a cost-effective, energy-efficient housing type. Credit: Next Step Network.