Window on the World

By Anthony Flint, August 12, 2024

Imagine having a giant dashboard that reveals buildings and open space and property ownership—all the critical components of the physical landscape, what’s happening literally on the ground, across cities and towns, rural areas, farmland, and forests.

That future has arrived, in the form of geospatial mapping, where technological advances have turbocharged the field. Analysts are using powerful computers, satellite imagery, and artificial intelligence to identify patterns and trends that inform land use policy decisions.

The technology allows local decision-makers to move more swiftly to develop effective policies and initiatives, according to Jeff Allenby, director of innovation at the Center for Geospatial Solutions, speaking on the Land Matters podcast.

“What excites me the most is how we have this power at our fingertips to really allow our partners to do more with the resources they have, the staff that they have, and the time that they have, and to get more to solving challenges versus just dealing with data management,” Allenby said.

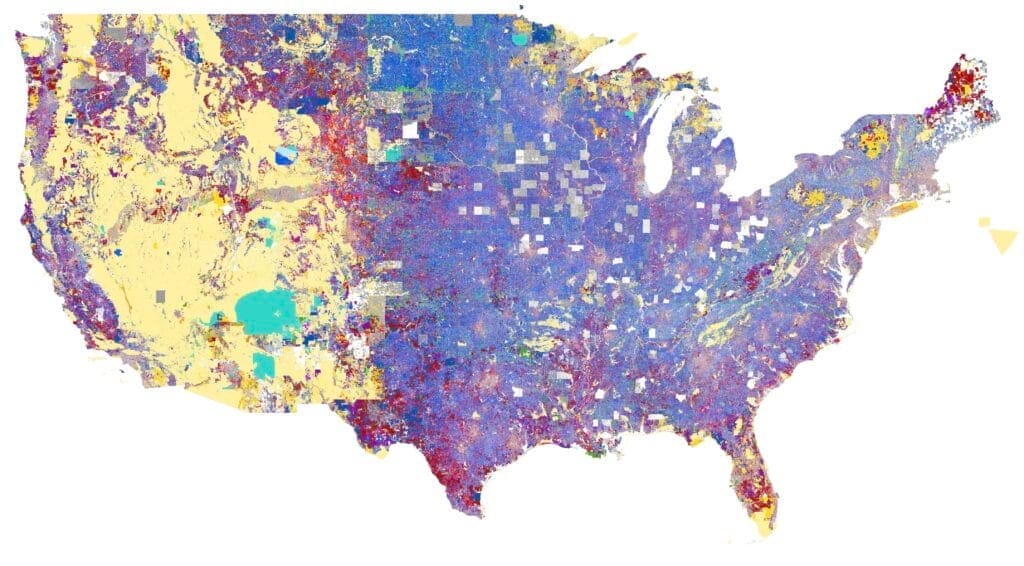

The utility of the work was evident recently as the Biden administration sought to encourage cities and towns to build more housing. The White House cited findings revealed by the Center’s innovative Who Owns America® analysis that catalogued land owned by local, state, or federal government entities in the US—and further identified the parcels that were actually available to be developed, in already settled areas and near some form of transit. A typical parcel was an unused parking lot or decommissioned public works garage; wetlands, parks, and other essential uses were excluded.

Analysts concluded that close to 2 million homes could be sited on the identified publicly owned land (about 276,000 buildable acres), which is equivalent to estimates of the housing supply shortage that is helping keep prices so high. That number would jump to nearly 7 million if the parcels were developed with more density.

Similar property ownership mapping efforts by CGS identified the amount of buildable land owned by faith-based organizations in Massachusetts and Arizona, to test the viability of the so-called “Yes in God’s Backyard” movement, which encourages housing development on land owned by churches, mosques, temples, and synagogues.

“The power of the Who Owns America analysis is that you can begin to ground some of these abstract policy conversations in reality and move from saying, ‘We want to develop religious-owned properties for affordable housing,’ to tangible steps to make it happen,” Allenby said.

Property ownership by institutional investors has also been a subject of investigation, as CGS examines the trend of corporate entities buying up houses and charging often-exorbitant rents, in legacy cities and elsewhere. By analyzing information like owner addresses, the CGS team can show how, in some cases, institutional investors have snapped up most of the homes across several blocks.

The team can set criteria and filters to look at the potential of a range of other land use elements, such as underperforming strip malls or enclosed shopping malls, unused parking lots, or brownfields, Allenby said. CGS can also show how tweaking local zoning opens up land for different kinds of housing, including two- to four-unit multifamily townhouses, accessory dwelling units, or manufactured homes, which are an affordable alternative to standalone single-family homes.

For more on the Center for Geospatial Solutions, which was founded at the Lincoln Institute in 2020, visit www.cgsearth.org.

Listen to the show here or subscribe to Land Matters on Apple Podcasts, Spotify, Stitcher, YouTube, or wherever you listen to podcasts.

Anthony Flint is a senior fellow at the Lincoln Institute of Land Policy, host of the Land Matters podcast, and a contributing editor of Land Lines.

Lead image: Mapping by the Center for Geospatial Solutions has identified government-owned land across the country that is suitable for potential development. Credit: Center for Geospatial Solutions.

Further reading

Building Where it Matters | Land Lines

Report: Development Opportunity on America’s Public Lands | Center for Geospatial Solutions

Will the White House’s Housing Plan Impact Utah’s Federal Lands? | Salt Lake Tribune

US Cities Map Investors Snapping Up Affordable Homes | Context

Yes in God’s backyard? This housing solution may be the answer to your prayers | Vox

Who Owns America: The Geospatial Mapping Technology That Could Help Cities Beat Predatory Investors at Their Own Game | Land Lines

Revealing Who Owns America | Land Lines

Mapping a More Efficient Approach to Land Use | Land Lines

Subscribe to Land Matters on Apple Podcasts, Spotify, Stitcher, YouTube, or wherever you listen to podcasts